The Mental Health Parity Laws define insurance coverage standards that require equal financial treatment for behavioral health and medical services. However, behavioral health providers experience reimbursement disparity.

The reimbursements are approximately 22% lower for behavioral health providers than for equivalent medical services. It reveals a gap between regulatory intent and payer execution.

The reimbursement gap in behavioral health is due to weak law enforcement and insurance policy loopholes that limit compliance effectiveness. Another structural issue is that insurance billing systems were originally designed for medical specialty workflows rather than behavioral health service models.

These gaps contribute directly to underpayment in mental health claims. Let’s discuss what you can do to protect your revenue.

What Do Mental Health Parity Laws Actually Require?

Mental health parity laws require health insurance plans to apply equal financial rules, treatment limitations, and coverage restrictions in the following:

- mental health services

- substance use disorder (MH/SUD) services

- medical and surgical services

The Mental Health Parity and Addiction Equity Act (MHPAEA) is the core federal parity legislation. This law replaced the Mental Health Parity Act of 1996. It turned out to be beneficial and closed several coverage loopholes.

Under MHPAEA, health plans that offer any behavioral health benefit cannot:

- Apply higher copays or deductibles to mental health care than to medical care

- Set stricter visit limits or inpatient day limits for mental health treatment

- Use more restrictive prior authorization, medical necessity review, or utilization management for behavioral health services

MHPAEA does not require plans to offer behavioral health coverage at all.

Why Reimbursement Rates Stay Lower for Behavioral Health Providers

Behavioral health providers receive lower reimbursement rates than medical/surgical providers. The reason is that laws require insurers to treat mental health services similarly to medical services. But they do not force insurers to pay the same dollar amount.

Consequently, behavioral providers are often paid less than their medical counterparts. Insurers set reimbursement rates based on different market strategies, not legal parity

According to a 2024 RTI International study:

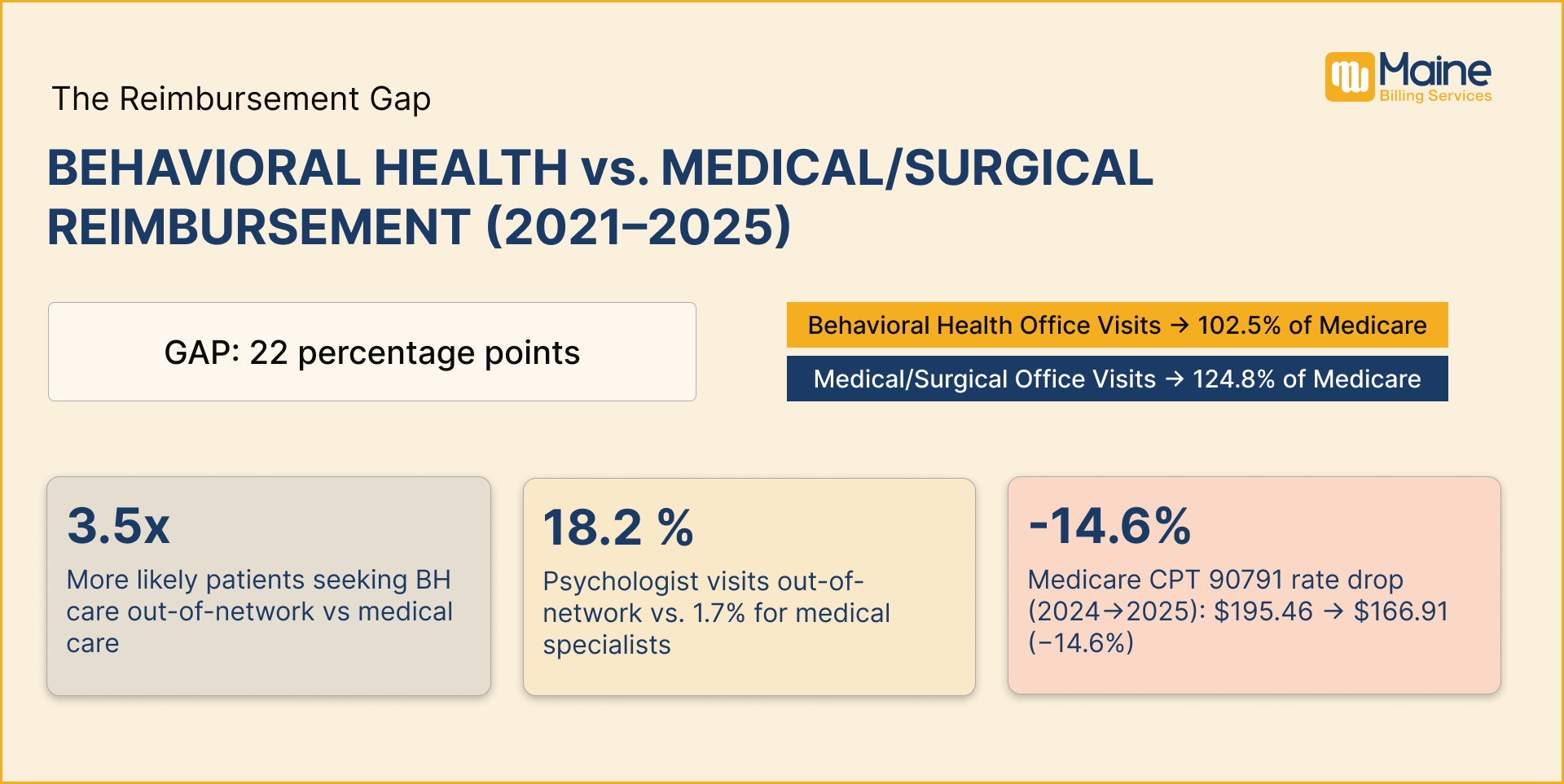

All medical/surgical clinician office visits averaged 124.8% of Medicare rates, while behavioral health clinician visits averaged just 102.5% of Medicare, a gap of nearly 22 percentage points.

That reimbursement gap has a direct consequence. Clinicians who can earn higher rates for medical/surgical services have less incentive to specialize in or remain in behavioral health. This contributes directly to the network adequacy crisis that affects providers and patients alike.

The behavioral health workforce is affected by lower pay compared to medical specialties, which reduces the incentive for clinicians to stay in the field. The healthcare access system faces provider shortages in mental health. It also contributes to the network adequacy problem for patients.

How Medicare Payment Cuts Are Reducing Revenue

The Medicare reimbursement system introduced lower mental health payment rates in 2025. It reduced reimbursements by nearly 14% compared to 2024. The major metro reimbursement markets, including Chicago, Miami, and Houston, experienced higher regional Medicare cuts exceeding 16% for mental health billing services.

The CPT Code 90791 reimbursement rate also showed a national payment decrease from $195.46 in 2024 to $166.91 in 2025.

The mental health practices with high Medicare volume face immediate revenue loss from this. This problem cannot be solved through parity appeals alone. It requires a fee schedule review, contract renegotiations, and volume adjustments.

How Insurers Violate Reimbursement Parity Rules

The parity laws do not require equal payment amounts between behavioral health and medical providers, but they do require equal reimbursement structures and calculation methods. The insurance reimbursement process becomes a parity violation when insurers use different methods to calculate behavioral health and medical provider payments.

Specific examples of methodology violations are the following:

- Reducing reimbursement rates for non-physician MH/SUD providers by a fixed percentage. That does not apply to non-physician medical providers

- Reimbursing behavioral health providers at Medicare rates while paying medical providers at 2x Medicare rates

- Applying different fee schedule structures

The payer reimbursement review process should compare payment structures across equivalent specialties to identify parity violations beyond the final dollar amount. That comparison is the core of a parity-based dispute.

Table: MHPAEA Requirements vs What Providers Actually Experience

| MHPAEA Requirement | What the Law Requires | What Providers Actually Experience |

| Prior Authorization | Same rules as medical services | More frequent and stricter approvals for behavioral health |

| Reimbursement Methodology | Same calculation method as medical providers | About 22% lower payments for behavioral health (RTI, 2024) |

| Network Adequacy | Enough in-network providers for access | Many behavioral health providers are unreachable or unavailable |

| NQTL Comparative Analysis | Must be provided within 10 days on request | Often delayed or initially incomplete in practice |

| Credentialing | Similar timelines as medical providers | Longer delays and more requirements for behavioral health |

| Medical Necessity Rules | Same standard as medical conditions | Stricter internal criteria for behavioral health claims |

| Out-of-Network Use | Should reflect adequate network access | Behavioral health patients go out-of-network more often |

Parity Violations, Appeals, and What Actually Works

The parity appeal process helps providers recover lost revenue from unfair claim handling by using MHPAEA rules and treatment comparisons.

Most billing teams first submit clinical appeals for denied claims to overturn payment rejections. But when a denial pattern shows a systematic difference in how behavioral health claims are treated compared to equivalent medical claims, the appeal needs to explicitly implement parity law.

- Check 12 months of denial data by reason code to find when behavioral health denials are higher than medical.

- Ask for the plan’s NQTL analysis. The CAA 2021 requires plans to provide this analysis within 10 business days.

- Compare a similar medical service for the same rules on authorization, denial rate, and coverage. Document your findings in writing.

- Use MHPAEA in your appeal letter to show unequal treatment and request equal process proof.

- Report unresolved parity issues to the Department of Labor or state insurance commissioner (Value).

Work With a Billing Team That Understands Behavioral Health

Stop leaving revenue on the table because of parity violations you are not pursuing.

Maine Billing Services provides behavioral health-focused revenue cycle support. Our team handles credentialing, prior authorization management, parity-based appeals, and claim submission, so you can focus on patient care, not insurance disputes.

Contact Maine Billing Services

Frequently Asked Questions

1. What is a parity violation in mental health billing?

A parity violation happens when insurance plans apply stricter financial rules or restrictions to behavioral health services compared to medical services. This leads to unfair reimbursement or claim denials.

2. Does MHPAEA guarantee equal payment for mental health providers?

The MHPAEA law requires equal rules for coverage and treatment limits. But it does not require equal dollar reimbursement.

3. Why do behavioral health claims get denied more often?

The behavioral health claims get denied more often because the insurance claims review system uses stricter utilization management and authorization requirements for behavioral health.

4. What is an NQTL analysis in simple terms?

The NQTL comparative analysis is a payer report. It shows how insurance rules are applied across services. It checks whether behavioral health is treated more strictly than medical care.

5. Can providers challenge underpayments from insurance companies?

Yes, providers can challenge underpayments from insurance companies by using MHPAEA rules, data comparison, and payer documentation requests